How Container Carriers Engineered Their Own Downturn

By: Spencer Graham

Mar. 9, 2026

In 2020-2021, shipping carriers saw the most profitable years in industry history. This increase in working capital could have been used to pay down debt or reinvest in the future. Instead, it went to ordering ships. The container shipping industry has a pattern of overordering ships during boom periods. Carriers chase capacity when profits are high, even though doing so often sets up the next market downturn.

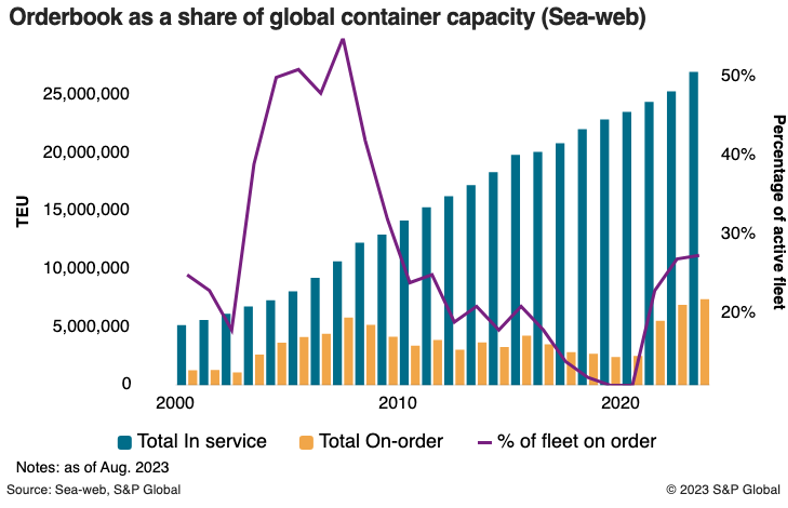

An order book is a dataset of all new ships currently ordered from shipyards but not yet delivered. Currently, the order book stands at 11.61 million TEU, representing 34.8% of the active fleet. But they aren’t doing this to meet demand. Fleet growth was 6.7% for 2025, while demand was only 2.6% for the year. The 633 ordered in 2025 surpasses records set in both 2021 and 2024. The industry is expanding capacity far faster than demand requires. It is growing at twice the rate of demand with no mechanism to stop it. This problem looks less like a miscalculation and more like overconfidence built into the industry's DNA.

The last time that the order book exceeded current levels was in 2004-2009. During this period, carriers continued to order ships to further expand their capacity. When the 2008 financial crisis hit, demand plummeted, but ships kept arriving.

The cycle peaked in the 2016 bankruptcy of Hanjin Shipping, the largest collapse in container shipping history. Ports refused its ships, cargo was stranded at sea, and supply chains around the world were disrupted.

The similarities in today's world are hard to ignore. Once again, carriers are ordering ships at a rate that has well surpassed their demand. The industry has been through this cycle before.

How is this time different?

In previous cycles, oversupply eventually corrected itself as aging ships were scrapped. That process helped absorb some of the capacity entering the market. This time, the industry is expanding the fleet while barely scrapping ships at all.

In a normal oversupply cycle, older ships would get scrapped, paving the way for the newer ships. Container ship demolition hit a 20-year low in 2025, with only 12 container ships being scrapped the whole year.

The result is a market where capacity is expanding from both ends. Carriers are adding ships at record levels while keeping older vessels in service. Instead of correcting the oversupply cycle, the industry may be amplifying it.

One reason the oversupply problem has not yet fully surfaced is the disruption in the Red Sea. Attacks on commercial shipping forced many carriers to reroute vessels around Africa rather than using the Suez Canal. These longer voyages absorbed excess capacity by tying up ships for additional weeks at sea.

The detours temporarily covered up the imbalance between supply and demand. With vessels spending more time on each route, fewer ships were available to carry cargo at any given moment. Roughly 10–15% of global container capacity has been tied up in longer voyages due to the Red Sea rerouting.

If Red Sea transit normalizes, that buffer disappears. Millions of TEU currently tied up in longer voyages would re-enter the market almost immediately, adding capacity to an industry that is already expanding faster than demand.

The current orderbook suggests the container shipping industry may be entering another familiar cycle. Capacity is expanding rapidly, while the normal mechanisms that would reduce excess supply remain largely inactive. Temporary disruptions, like the Red Sea rerouting, have helped carriers justify their increased need for more ships. But they have not solved the underlying imbalance.

For cargo owners and manufacturers, the coming years could bring a return to cheaper freight rates after the volatility of the pandemic period. For carriers, the outlook is less favorable. The pandemic offered a rare opportunity to strengthen balance sheets and reduce this cycle. Instead, carriers reinvested heavily in new supply, which may now shape the next decade of the container shipping market.